Aldi and Lidl: Food Retailing Innovation or Just Keeping Up With Shoppers?

Typically, with the advent of a new year comes a wave of stories featuring trends and predictions on just about anything imaginable. We’re early into 2018, and while these types of stories are plentiful, a couple of big newsmakers from a year ago have carried over and grabbed their share of headlines on the food retailing front.

Typically, with the advent of a new year comes a wave of stories featuring trends and predictions on just about anything imaginable. We’re early into 2018, and while these types of stories are plentiful, a couple of big newsmakers from a year ago have carried over and grabbed their share of headlines on the food retailing front.

The implications of the expansion of discounters Aldi and Lidl continue to be a much-discussed topic while industry analysts, pundits and players keep an ever-watchful eye on what Amazon’s acquisition of Whole Foods Market portends for the coming months.

In a remodeled store near its U.S. headquarters in Illinois, Aldi unveiled a heightened in-store experience concept that features positioning an in-store bakery and fresh produce department at the front of the store. While this is strictly a pilot program in only that store, according to Aldi, the news struck a familiar note with us. In mid-September 2017, we made the following observations about Lidl’s entry into the U.S. marketplace:

“The important sensory reality of Lidl’s entrance is that bakery, produce and flowers are all within ten feet of the shopper. ... Produce was prominently featured up front with some stores displaying melons and others English cucumbers. Where Lidl’s entrance experience stands apart from its American competitors is the innovative location of bakery right up front inside the entrance. In Whole Foods Market, the gold standard for high-quality food experiences, you must walk a good distance into the store to find the bakery. In Lidl stores, the bakery is on the left as you walk in.”

Coincidence? We don’t know. While it’s often said that imitation is the sincerest form of flattery, we think it’s likely Aldi has been listening to criticisms of its stores as utilitarian. This is how we compared Lidl to a traditional Aldi entrance experience:

"By contrast, the entrance at Aldi is a funnel of packaged, processed food “deals” and strikes a very different tone with the shopper. From our perspective, Aldi has accidentally reinvented pantry stocking in America by subversively eliminating the variable brand and the shopper marketing that goes along with it. Aldi has also eliminated the variable of price, for there are no price comparisons in a store with only one offering in every category. An Aldi shopping trip is therefore radically simpler: no thinking about brands, BOGOs, deals, price comps, coupons, sudden endcap promotions or in-aisle shopper marketing.”

An in-store bakery is certainly not a new concept. The aroma of fresh-baked goods wafting through the store has been a staple of mainline grocery stores in the U.S. marketplace for decades. In many ways, the Aldi test of fresh, higher-quality experiences underscores how hard discounters like Aldi and Lidl are learning to compete in the American market. They know that by providing cues to quality and freshness (e.g., organics, "gourmet" SKUs, in-store bakery and fresh produce), they can take on not only Walmart but traditional food retailers.

What’s really going on here?

While the media and analysts are focused on what these companies are doing (or not doing) to physical aspects of the store, there is a much more important element to consider, one that The Hartman Group has been laser-focused on from our earliest days: consumer culture.

While the media and analysts are focused on what these companies are doing (or not doing) to physical aspects of the store, there is a much more important element to consider, one that The Hartman Group has been laser-focused on from our earliest days: consumer culture.

We know there is a fundamental shift occurring in the marketplace. With the continued blurring of channels, some traditional retail venues are rapidly losing relevance, quite simply because they are not keeping up with a changing shopper and shopping culture.

The shopping universe is no longer dictated by manufacturers and retailers — and the power is being transferred to shoppers. The shopper doesn’t just desire to be more in control of his or her own destiny, they increasingly recognize that they are in control.

Optimistic and empowered with a shield of unprecedented access to information, they are now increasingly in control of their ability to make choices about how and where they shop and are driving this change. We’re standing on the threshold of an uncertain future, faced with a number of critical questions.

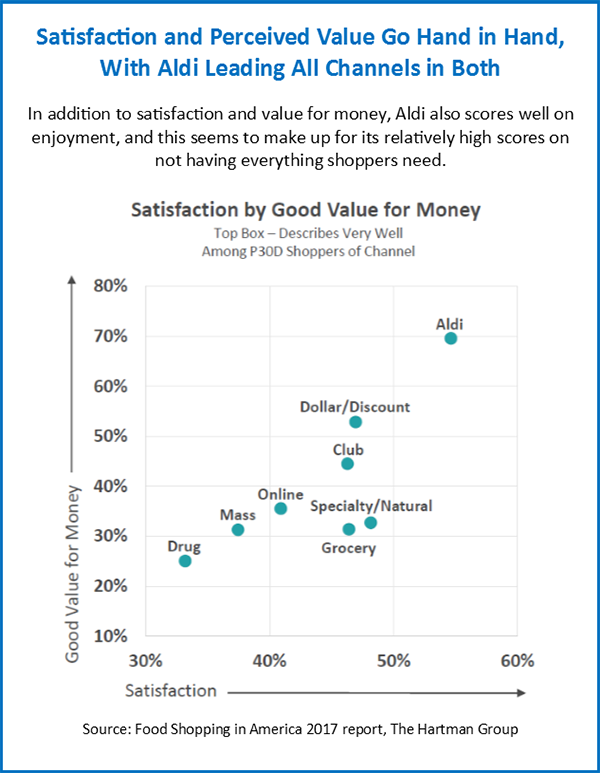

Our Food Shopping in America 2017 report finds that in response to new formats in both physical and virtual food retailing, shoppers are developing complicated shopping routines in the name of providing the right foods for their households at the best value. Complicated shopping routines mean that shoppers are cross-shopping among channels more than ever before. This includes shoppers picking and choosing from retailers that fall within Grocery, Mass, Drug, Club, Specialty/Natural, Discount/Dollar, Small Footprint/Fresh Format and Online types.

Pertinent to the aggressive plans for growth that both Aldi and Lidl have signaled for the American marketplace, we find that retailer growth in grocery is highest among specialized players, which underscores an excellent argument for grocers to focus on retail strengths.

In the report, our analysis finds that Aldi outpaces all channels on growth, and with Lidl's entrance to the U.S. market, it is likely to significantly contribute to ongoing disruption in grocery-shopping behaviors. Aldi shoppers love the combination of low prices, high-quality items and even the limited choices (finding it easier to shop than a typical store). Grocery, Mass and perhaps even Club should watch this fast-growing competitor carefully, and Aldi should keep a close eye on how Lidl may change the grocery landscape.

This is a story that continues to be written, and we will be staying close to consumers to monitor their response to a very fluid, rapidly evolving and exciting food retailing marketplace.

To download your copy of our white paper on Lidl, click here.

To learn more about the Food Shopping in America report and how the food retail landscape and grocery shoppers are changing, click here.

For our take on ALDI, click here