A Third Grocery Sector: The Rise of Refrigerated Packaged Foods

The average U.S. home has more freezer space than homes in any other nation; so why do frozen food sales continue to decline so rapidly even after the recession? There are many demographic reasons (e.g., the emptying of Boomers' nests), but a less discussed one is the rise of the refrigerated foods marketplace. Hartman Strategy calls it the Third Grocery Sector, and it lives at the intersection of two worlds: the extended shelf life found in center-store packaged foods and the high-quality taste and texture of fresh perishables.

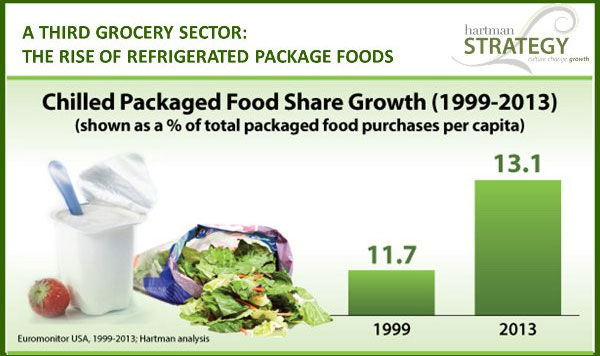

Chilled packaged foods have gained market share over the past 14 years, while the overall packaged food sector saw market share decline.

The frozen foods business was built on replacing low-stakes home meals (Swanson and Stouffer's), then the low-stakes U.S. work lunch (Lean Cuisine, Healthy Choice). "Because of this eating-occasion bias, frozen food was able to generate strong growth despite merely 'good enough' quality — setting the table for a long-term fall," said James Richardson, Senior Vice President of Hartman Strategy.

When the recession hit, consumers began to re-evaluate their spending priorities, especially in food. Not everyone traded down to cheaper frozen brands. Some consumers, especially more educated ones, traded out of the category and up to higher-quality, fresh alternatives — leading to strong growth for fast-casual restaurants and refrigerated entrées, sushi and salad right through the recession. In other words, consumers stopped settling for lower-quality frozen food as their awareness of higher-quality alternatives increased.

Refrigerated foods have been among the few large growth sectors in the grocery marketplace over the past 15 years, not much affected even by the recession. In fact, while overall per capita volumetric consumption of fresh and packaged foods has remained steady, the Third Grocery Sector has grown its share of stomach substantially.

In addition, after years of recessionary decline, volumes in the fresh grocery perimeter are growing again at a furious clip — seafood at 7.5 percent, delis at 4.3 percent and produce at 4.1 percent (courtesy of Nielsen), a strong sign that refrigerated packaged foods in and near those areas are riding a mega-trend toward fresh, higher-quality food experiences.

Historically, the Third Grocery Sector covered an array of seemingly disconnected foods: yogurt, bagged salads, Lunchables, retailer-packed leftovers from the deli's prepared foods counter, Lloyd's marinated beef, Hormel party trays and so on. That is changing, and it is important to consider the new reality supporting the area's growth: Consumers have great experiences in the deli, meat, seafood, produce and other perimeter sections of upscale grocers such as Whole Foods Market — and actually pay to attend their cooking classes. Trader Joe's has been incubating an enormous refrigerated salad and entrée business with almost fanatical devotion by its heavy users, who have largely abandoned frozen entrée buying as a result. Rather than focus exclusively on ultra-convenience or price plays, such grocers have brought the flavor and experiences necessary to compete with the quick-serve and casual-dining universe, thereby winning on both nutrient density and culinary credentials.

Hartman Strategy believes many CPG players, especially those in frozen foods, should develop a Third Grocery Sector strategy, if they haven't already. It is an area with relatively little competition — Tyson, WhiteWave, Campbell's and Hormel being among the few big players — waiting to be tapped.

To learn how your organization can benefit from decades of research and insights, please visit Hartman Strategy.

Contact:

Blaine Becker

Senior Director, Marketing

425.452.0818, ext. 124

blaine@hartman-group.com