Premium Development Trend: A Category-Specific Phenomenon

If you’ve been following our newsletter, then you know just how bullish we’ve been about the premium market. In recent years, we’ve been tracking the pace of M&A in the premium sector of the packaged food and beverage industry. During this time, we’ve witnessed more CPG firms making moves in this space than ever before. It signals a deepening acceptance that emerging premium brands are, on average, far outperforming legacy ones in driving sustainable growth.

If you’ve been following our newsletter, then you know just how bullish we’ve been about the premium market. In recent years, we’ve been tracking the pace of M&A in the premium sector of the packaged food and beverage industry. During this time, we’ve witnessed more CPG firms making moves in this space than ever before. It signals a deepening acceptance that emerging premium brands are, on average, far outperforming legacy ones in driving sustainable growth.

In previous issues of this newsletter, we’ve provided an understanding of how premium operates, culturally and financially, through the lens of specific category examples. Why? Because to win strategically over the long term, food businesses must be analyzed at the category level first.

In this issue, we further this deepening understanding of the burgeoning premium landscape through an analysis of specific food categories with very different premium market performance and very different positioning in modern food culture.

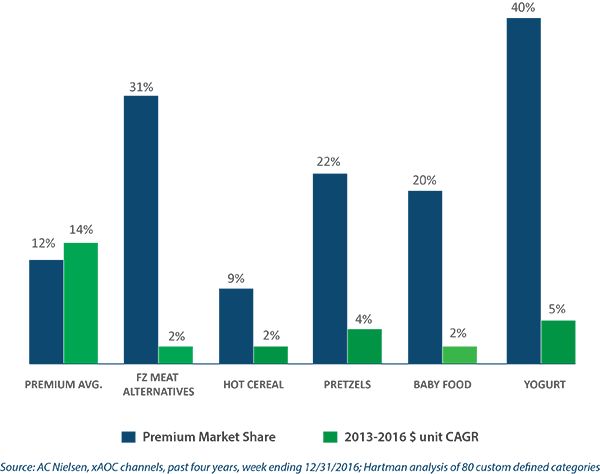

Premium Maturing: A Category-Specific Phenomenon

Premium is starting to mature in specific food categories: frozen meat alternatives, hot cereal, baby food, yogurt and pretzels. The following chart illustrates the results of recent AC Nielsen data we've reviewed for these categories. They've each attained average or above-average market share, but 2013-2016 unit CAGR is at or below 5 percent (after years of double-digit growth).

Hartman Analysis: Categories Where Premium Is Showing Signs of Maturing

|

Why? Is the $74 billion premium market maturing early? Not in our view. What is happening is a category-specific phenomenon.

For many, these categories are ones where innovation potential itself is weak, so purity was the basic innovation platform — and the only one. These categories are not culturally oriented to culinary innovation or significant health innovation. This has less to do with the technical potential for innovation than it does with the way these foods are encoded with specific kinds of low-stakes eating occasions in mind. We anticipate more low-stakes categories will see growth decline in the next five years.

At the same time, in categories that connect to higher-stakes eating occasions where technical innovation continues to be both possible and desired (e.g., yogurt), we expect to see the definition of “premium” be reframed culturally. This becomes the cultural equivalent of a stock split.

In these categories, declining unit CAGR augurs a redefinition of what premium is (and what drives the highest unit pricing). We anticipate this redefinition may further move yogurt toward minimal processing, particularly regarding no additives, non-GMO and very low sugar content.

Advanced Analytics Point the Path Forward

This market continues to confound and to defy simple generalizations. The importance of being a category expert for premium strategy only grows as the market grows.

Over the past three years, The Hartman Group has spent considerable time studying random samples of early-stage brands at different revenue hurdles and researching what go-to-market best practices are shared among various classes of successful brands.

Our analysis reveals that, while there are multiple routes to scale, product design, in the historical context of a specific operating category, is perhaps the most underdiscussed predictor of long-term growth past $100M. The key, we believe, is to understand which early-stage players have stumbled onto blinding white spaces for underserved innovation and invested in them early on.

![shutterstock_342248153-[Converted]](http://www.hartman-group.com/img/hartbeat/hand-holding-chart-100.jpg) Check out our PREMIUM M&A proprietary tools that focus on long-term growth and health, not short-term gains.

Check out our PREMIUM M&A proprietary tools that focus on long-term growth and health, not short-term gains.

Contact us to learn more about ways we can help you win in the dynamic premium marketplace.