Fragmented grocery market means consumers seek guidance from trusted retailers

It’s not just the mainstream usual suspects needing to answer the wake-up call regarding the consumer-led revolution around food and beverages. When Whole Foods’ future revenue growth is questioned and investors suggest the chain might be peaking, it’s clear that the consumer-driven changes to food retail are far from over.

The changes are not capricious or unpredictable. They’re tied to underlying cultural forces that, once understood, open up new opportunities for retailers who until now have experienced upheaval and whiplash.

A hallmark of the latest shift in food culture is how fractured grocery shopping has become, according to the Food Marketing Institute’s “U.S. Grocery Shopper Trends 2014,” an annual review conducted by The Hartman Group.

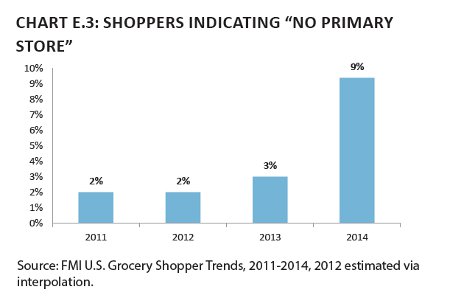

“What is most interesting is the leap in the number of people who claim they have no primary store. When FMI first started listing this option in 2011, only 2 percent said they had no primary store. This year, 9 percent claim no primary store,” said FMI President and CEO Leslie Sarasin.

This year’s study is particularly interesting, because it approached the research through a cultural lens, interviewing Americans in their homes and while shopping.

Hartman Group CEO Laurie Demeritt explains what that approach uncovered: “Drawing on ethnographic research, we found that the convenient, formerly helpful idea of a ‘primary shopper’ — a single adult responsible for, or at least knowledgeable about, an entire household’s grocery purchases — no longer does justice to how American households manage their food purchases.”

One result is what she calls “the roadside pantry”: food is everywhere, and people are buying it everywhere rather than being loyal to a single, primary store. In other words, it’s not that consumers are shifting loyalty on a permanent basis from supermarkets to supercenters or specialty retailers like Whole Foods. They’re shopping around, buying some items at one place and some at another — and another, and another — on an ongoing basis.

The fragmentation of the role of “primary shopper” also means that more men are shopping for food, and they shop differently from women. Only 52 percent of men create a list before shopping and fewer than half look at store circulars, gather coupons or even think about what they want to eat for certain meals and snacks before shopping. That compares with 69 percent of women who create a list and half or more who take part in the other activities.

The youngest adults, Millennials, also shop differently. They wait until the last minute to make lists and base them more on recipes and meal planning than on specials or what’s stocked at home.

In the bigger picture, health and wellness has become an integral part of food culture rather than the alternative movement it used to be. That means consumers increasingly look for foods and beverages that are minimally processed, are locally grown or produced and contain a short list of ingredients that they recognize.

It also opens up new opportunities for retailers, who can become consumers’ trusted allies by curating their products and communicating about them in a way that connects with people who have similar values. Retailers are uniquely able to help shoppers navigate the increasingly complex world of food and wellness.

Lunchtime continues to be a clear area of opportunity for grocery stores, beyond the “packed lunch” crowd. Lunch accounts for 59 percent of all meals eaten away from home, but 63 percent of those lunches are sourced from food service. If convenience priorities can be satisfied – for example, speed and away-from-home meal preparation — then retailers will be well-situated to address the midday mix of wellness needs.

Another way to connect is via nutritional labels. Consumers see retailers as their advocates in figuring out which products are best for their needs, and labeling programs communicate that information.

Retailers also have a host of other opportunities to connect with changing shoppers: offering product selection and services that cue health and wellness, capitalizing on meal occasions, sharing nutrition information and many other activities create bonds with today's consumers.

Questions or comments? Contact Blaine Becker at: blaine@hartman-group.com