Walmart and ALDI and Lidl, oh my!

With intense emphasis on low prices, shopping for food in America is about to get a whole lot more interesting — and competitive

Look out, America. A pair of German discounters is poised to greatly expand their footprints across our nation’s cluttered food-retailing landscape. While the threat of a looming price war might be sweet music to consumers’ ears, it’s not a tune U.S. food retailers want to be playing — but one they may be forced to quickly learn if they have any hope of retaining market share.

To stave off the aggressive growth plans announced by German discount retailers ALDI and Lidl, Walmart, for one, is retooling its deep-discount pricing strategy. But is low pricing alone enough for shoppers?

We’ve documented the threat of ALDI and how it has accidentally reinvented pantry stocking in America by subversively eliminating the variable brand and the shopper marketing that goes along with it. ALDI has also eliminated the variable of price, for there are no price comparisons in a store with only one offering in every category. An ALDI shopping trip is therefore radically simpler: no thinking about brands, BOGOs, deals, price comps, coupons, sudden endcap promotions or in-aisle shopper marketing. ALDI’s smaller-footprint stores also make for a quick shopping trip.

As we concluded in our past assessment of the ALDI shopping experience, ironically, the only variable left in the shopping trip is: the food. This a powerful disruption for highly utilitarian shopping trips where shoppers just want to get the stuff on their list and get out.

During our "Great Recession" (circa 2008), a good deal of discussion centered on how Americans were going to rapidly "trade down," and big things were predicted for low-price-driven retail formats that sold groceries as shoppers theoretically flocked to discounters like Walmart and Dollar General. Instead, consumers seemed to enjoy including yet more discount options in their ever-broadening food-shopping habits and, rather than embrace any one "kind" of retailer, chose to shop all types of food retailers, ranging from discount to fresh-format premium — and everything in between.

In 2012, in our Shopping Topography report, we documented how the consumers’ path to purchase, across all channels, has become more complex and multifaceted and has logistically veered off its previously well-traveled route.

Which brings us to today’s shoppers.

The single biggest narrative underlying grocery shoppers’ evolving behavior is their belief that their lives are “more chaotic and hectic than ever before.” Increasingly, consumers want to use their time in more compelling ways than for basic shopping and preparing food.

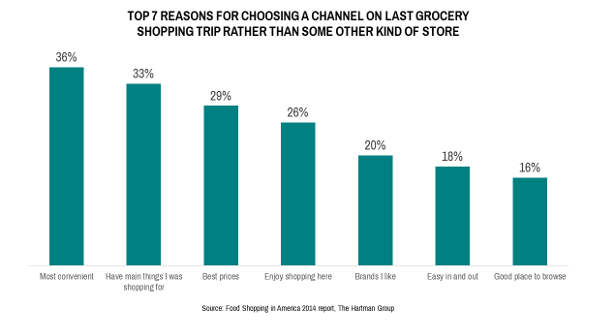

As consumers continue to struggle with money and time constraints, retailers that are the “most convenient” and have the “best prices” are more attractive than ever before. Convenience is a key determinant of store traffic, whereas price continues to be an important factor in food-purchase decisions.

The chart above shows that the top category drivers for choosing a store are convenience, overall product selection and price, but none of these alone is sufficient to fully engage consumers or build long-term brand equity. Shopping experience and relevance are also key and especially important in connecting with consumers.

Certainly ALDI and Lidl are just the tip of the iceberg in what is a mounting and turbulent sea of discount-grocery options for consumers now able to shop from unbounded horizons when it comes to purchasing foods and beverages, or what we’ve often called the “roadside pantry effect.”

The roadside pantry effect is the concept that consumers now navigate a world of 360-degree food availability, picking and choosing from a huge pantry of physical as well as virtual options. This is a much larger concept than the often-heard “multi- or omni-channel shopper.”

With all the existing and emerging possibilities, grocery shopping will continue to change dramatically. What does food shopping in America look like in 2017? What will it look like in a couple of years?

To remain relevant and competitive, companies today must also evolve and reinvent themselves. Some key questions to ask:

- How well do we know our consumers’ shopping habits and preferences?

- Are we attracting and engaging with our target consumers?

- What assortment and offerings would be more relevant?

- What technologies and innovations would best enhance the customer experience and drive retention?

The retail environment is more competitive and dynamic than ever before. As Walmart, ALDI, Lidl and all the other players in the food-retailing arena need to understand, those who successfully understand and satisfy consumers’ complex needs will be the most effective in building long-term trust and loyalty.

The retail environment is more competitive and dynamic than ever before. As Walmart, ALDI, Lidl and all the other players in the food-retailing arena need to understand, those who successfully understand and satisfy consumers’ complex needs will be the most effective in building long-term trust and loyalty.

Take the first step in developing this new understanding. Sign up today for The Hartman Group’s important new research, Food Shopping in America 2017.