Premium Is About Marketing to Niches

As more and more CPG firms purchase emerging premium brands to balance their portfolios, more and more executives are coming to terms with the limitations of traditional performance indicators and definitions of success inside their enterprises.

As more and more CPG firms purchase emerging premium brands to balance their portfolios, more and more executives are coming to terms with the limitations of traditional performance indicators and definitions of success inside their enterprises.

Traditional definitions of success in growth initiatives center on charging hard for large Y1 revenue-creating product launches, usually brand or line extensions.

In order to accomplish this so quickly, it is almost necessary to go national very broadly and be acceptable to a large number of potential households. Maximizing trial is the key to success in this default approach.

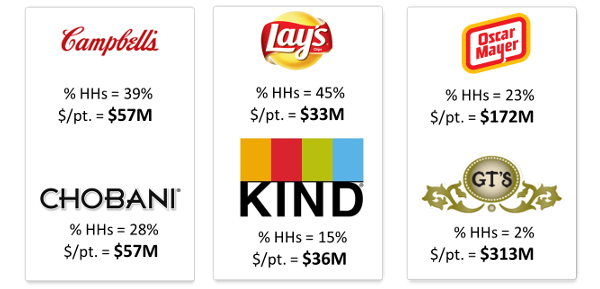

But, with premium brands, what we are finding is that enormous scale is possible with very limited household penetration. In fact, our recent work is suggesting that successful premium food and beverage brands can generate as much revenue per point of household (HH) penetration as 100-year-old legacy food brands selling to far more households.

Let’s take a look.

Source: Euromonitor, 2016, and Hartman Penetration Surveys; Hartman analysis

In other words, premium brands, because they have highly differentiated product designs, activate highly lucrative household/consumer niches for the benefit of the broader portfolio.

The largest premium brands, selling $400M+ annually, have an average HH penetration of only 16%, far lower than large legacy brands. You can even reach $1B in sales without hitting one-third of American households.

Premium food marketing is about scaling within subpopulations using clever product design and generating high buy rates per household. The more disruptive and tailored the product, the greater the apparent loyalty.

Undifferentiated, easy-to-mass-market products do not generate stickiness and require large household penetration brands to generate trial revenue…which often does not yield sustained repeat purchasing.

Premium. It’s about scaling within niches…